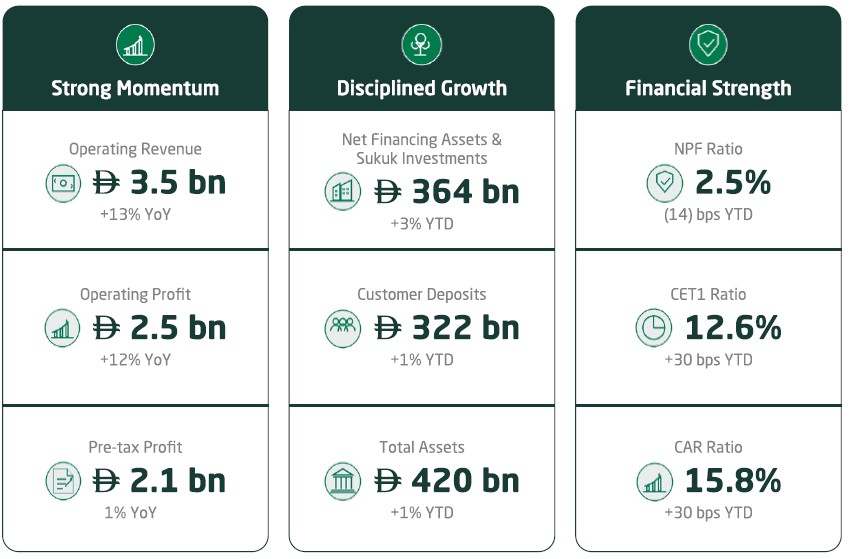

DIB (DFM: DIB), the world’s leading Islamic financial group and the largest in the UAE, delivered a solid start to 2026, supported by broad-based business momentum and disciplined balance sheet management. The Bank recorded 13% year-on-year revenue growth, with Q1’26 operating revenues of AED 3.5 billion, while total assets reached AED 420 billion. Strong Performance was underpinned by 12% YoY growth in Operating Profit reflecting highly efficient franchise, 3% YTD growth in financing and sukuk investment portfolio, further strengthening in asset quality with NPF ratio improving to 2.5% and stronger capital levels, supporting sustainable growth and returns.

Key Q1’26 Performance Metrics:

Performance Highlights for Q1’26:

Income Statement::

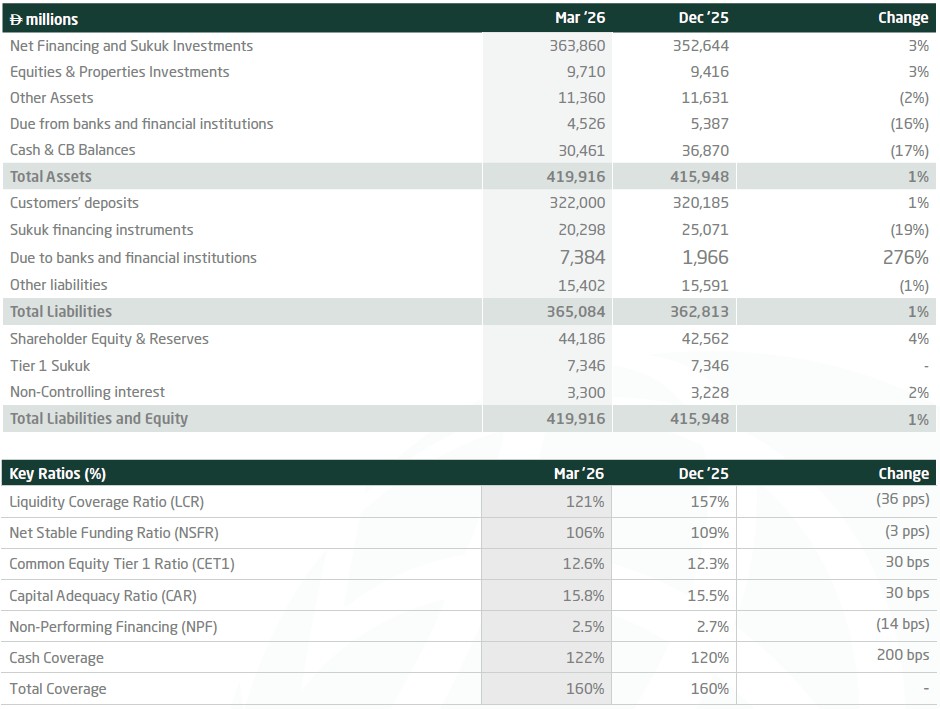

Balance Sheet:

Asset Quality:

Capital:

Liquidity:

His Excellency Mohammed Ibrahim Al-Shaibani, Director-General of His Highness The Ruler’s Court of Dubai and Chairman of DIB

“The first quarter of 2026 has once again shown the strength of the UAE’s foundations and the confidence that its economy continues to command, even as regional developments shape a more watchful external environment. What distinguishes the UAE in times such as these is not only the resilience of its economy, but the clarity of its leadership, the strength of its institutions and the readiness of its policy framework to preserve stability, support growth and maintain confidence across the system. The measures announced by the Central Bank of the UAE during the period are a further reflection of that preparedness and of the soundness of the country’s financial sector architecture.

Against this backdrop, DIB’s Q1 performance reflects the benefits of scale, discipline and strategic consistency. The Bank continues to operate from a position of strength, with net financing assets and sukuk investments reaching AED 364 billion and customer deposits standing at AED 322 billion by the end of the first quarter. These are not only indicators of scale; they reflect the strength of the franchise, the confidence of our customers and our ability to continue supporting economic activity with prudence and purpose.

DIB’s role has always extended beyond financial performance alone. As a leading institution in the UAE and in Islamic finance globally, the Bank remains committed to supporting the real economy, enabling opportunity across sectors, and contributing to the long-term ambitions of the UAE through a model built on strong governance, sound risk discipline and responsible growth. The task ahead is not simply to preserve strength, but to deploy it well, with prudence, purpose and a clear commitment to supporting the UAE’s progress while building enduring institutional value.”

Dr. Adnan Chilwan, Group Chief Executive Officer of DIB

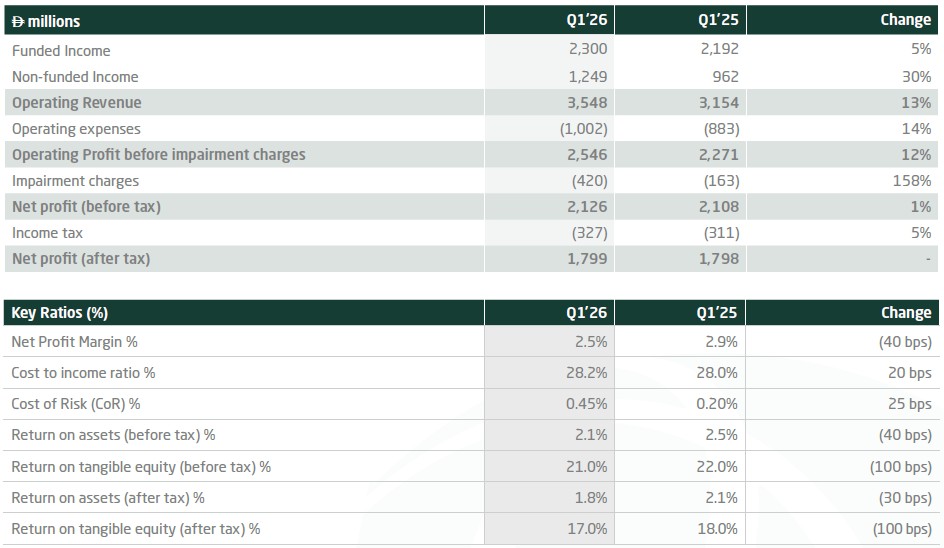

“DIB delivered a strong start to 2026, with operating revenue rising to AED 3.5 billion, up 13% year-on-year, and pre-tax profit reaching AED 2.1 billion. The quarter reflects healthy business momentum, improving earnings diversification and the continued strength of the Bank’s core franchise.

Our revenue profile continued to broaden during the quarter. Funded income increased by 5% year-on-year, while non-funded income grew by 30%, reflecting stronger contribution from across the business and a more balanced income mix overall. This helped drive operating profit to AED 2.5 billion, while pre-tax return on tangible equity remained strong at 21%, in line with our focus on quality growth and sustained profitability.

Balance sheet expansion remained healthy and well supported. Net financing assets and sukuk investments grew to AED 364 billion, supported by more than AED 24 billion in gross new financing and over AED 5 billion in gross new sukuk investments during the quarter. Customer deposits rose to AED 322 billion, reinforcing the depth of our funding base and providing solid support for continued business growth.

Asset quality also continued to improve, with the non-performing financing ratio declining to 2.5%, while cash coverage strengthened to 122%. These metrics reflect the quality of our underwriting, the effectiveness of our risk discipline and our continued focus on preserving balance sheet strength as we grow.

That same prudence continues to shape the way we manage risk. Our provisioning approach, including the addition of management ECL overlay where appropriate, reflects a deliberate and disciplined stance towards risk, while supporting the long-term resilience of the Bank.

Our capital and liquidity positions also remained sound, with CET1 at 12.6%, capital adequacy at 15.8%, LCR at 121% and NSFR at 106%. This leaves us strongly positioned for the periods ahead, with the financial strength, commercial momentum and execution discipline to keep advancing our growth agenda without compromising the quality of the franchise.”

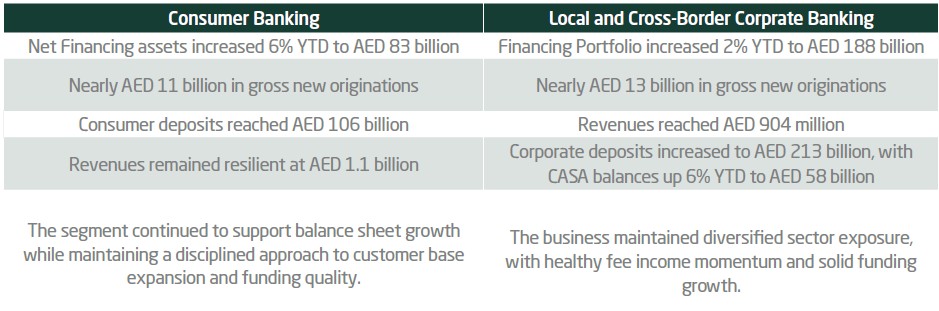

Business Segment Highlights:

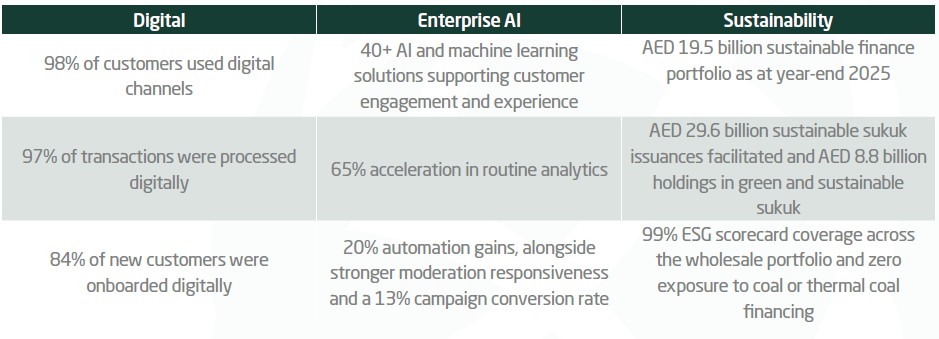

Progress Across Key Strategic Priorities:

Alongside its financial performance, DIB continued to make progress across digital banking, enterprise AI and sustainability. The achievements below provide additional context on the Bank’s progress across key strategic priorities beyond the quarter’s core financial performance.

Financial Review: Income Statement:

Profitability and prudence:

Financial Review: Balance Sheet

Strength and resilience:

DIB Successfully Issues Debut Sustainability-Linked Financing Sukuk

DIB and HCLTech Forge Strategic AI Innovation Partnership