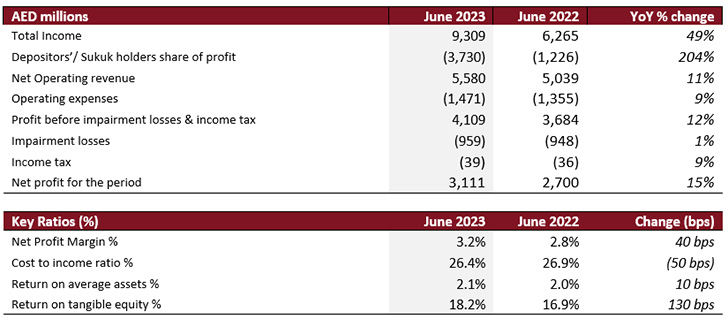

- Total Income rises by 49% YoY to AED 9.3 billion.

- Net profit of AED 3.1 billion, strong growth of 15% YoY.

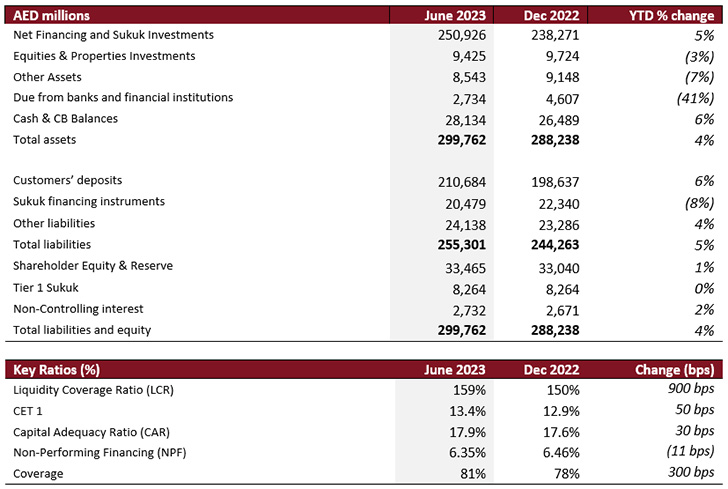

- Balance sheet expansion of 4.0% YTD to nearly AED 300 billion.

- Continued improvement in RoTE registering 18.2%, up 120 bps YTD.

Dubai Islamic Bank (DFM: DIB), the largest Islamic bank in the UAE, today announced its results for the period ending June 30, 2023.

1H 2023 Highlights:

- Group Net Profit came in at AED 3,111 million, up 15% YoY compared to AED 2,700 million. Growth was driven by rising core revenues, controlled impairments and effective cost management.

- Net financing and sukuk investments at AED 251 billion, up 5.3% YTD. Gross new underwriting and sukuk investments during 1H 2023 reached AED 45 billion vs AED 33 billion in 1H 2022.

- Total income reached to AED 9,309 million compared to AED 6,265 million, a solid expansion of 49% YoY.

- Net Operating Revenues showed a robust 11% YoY to reach AED 5,580 million.

- Net Operating Profit now at AED 4,109 million, a 12% increase YoY compared to AED 3,684 million in 1H 2022.

- Balance sheet expanded by 4.0% YTD to nearly AED 300 billion.

- Customer deposits increased to AED 211 billion with CASA comprising 39% of DIB’s deposit base. The high rate environment has led to investment deposits increasing its contribution to total deposits to 61% from 56% in YE 2022. CASA has shown an improving trend QoQ growing by AED 1.5 billion.

- Impairment charges registered AED 959 million against AED 948 million in 1H 2022, marginally up by 1.2%. However, 2Q 2023 impairments are down 7% QoQ and 13% YoY.

- NPF drops to 6.35% compared to 6.46% FY2022, lower by 11 bps.

- Cost to income further improved to 26.4%, down 50 bps YoY.

- Liquidity remains healthy with LCR at 159%.

- Continued improvement on ROA now at 2.1% (+13 bps YTD) and ROTE at 18.2% (+120 bps YTD).

- Capitalization levels remain robust with CET1 at 13.4% (+50bps YTD) and CAR at 17.9% (+30bps YTD), both well above the minimum regulatory requirement. Total equity now stands at AED 44 billion.

Management’s comments for the period ending 30th June 2023:

His Excellency Mohammed Ibrahim Al Shaibani, Director-General of His Highness The Ruler’s Court of Dubai and Chairman of Dubai Islamic Bank

- Amidst moderating global growth, the UAE economy continues to expand driven by recovering tourism, real estate and rising financial markets. With Dubai alone welcoming more than 8.5 million visitors in the first half and with DFM rising by 14% year to date, this clearly indicates a strong domestic economy supported by the UAE’s non-oil sector which is estimated to grow at above 4% this year.

- The banking sector continue to remain resilient with rising profitability, strong and growing credit and deposit portfolio supported by the private sector, GREs as well as the retail sector. This expansion is reflected in a continued upward momentum on PMI levels, growing domestic population and increasing FDI inflows.

- A strong set of first half results with total income reaching AED 9.3 billion up 49% YoY with rising profitability ratios on ROA and RoTE is a clear indication of the bank’s robust financial position, improved cost efficiencies and strong growth across its consumer and corporate business portfolios.

Dr. Adnan Chilwan, Group Chief Executive Officer

- Dubai has been on a remarkable recovery path during the first half of the year with most key sectors depicting strong levels of growth. Additionally, the Dubai Financial Market rose by 14% YTD mirroring the resilience of the Emirate’s corporates. The various business and economic reforms placed in by government have reinforced Dubai as a leading global city and DIB’s strong first half results clearly shows that the bank is at the forefront of supporting the national growth agendas.

- Sectors such as tourism, construction, real estate and investment in clean energy provide tailwinds to an expanding non-oil economy further reiterating DIB’s strategic alignment to the UAE’s expansionary agenda.

- DIB’s profitability during the first half has once again been notable with net profit reaching AED 3.1 billion, up 15% YoY, reflecting higher revenues, controlled costs and impairments and a keen focus on executing our medium-term strategic objectives.

- We have reached another key historic milestone as the bank’s balance sheet has now reached AED 300 billion, a strong rise of 4% YTD. The financing book grew by 2% YTD to AED 190 billion across corporate and consumer and further reinforced by a surge in our digital sales and transactions particularly on the consumer business. Including Sukuk, the bank has grown 5.3% well ahead already of the full year growth guidance.

- DIB’s gross new financing and sukuk underwriting of AED 45 billion during the quarter was up by a considerable 36% compared to AED 33 billion in 1H2022 fueled by corporate and retail lending underpinning DIB’s strong market position and business appetite for growth.

- The fixed income book grew by an astonishing 18% YTD and 31% YoY now reaching at AED 61 billion from AED 52 billion in FY 2022. The portfolio is primarily invested in highly rated sovereign instruments across the region.

Financial Review:

Income statement summary

Balance Sheet Summary

Operating Performance

The bank’s Total Income rose to AED 9,309 million in 1H 2023 demonstrating a notable YoY growth of 49% compared to AED 6,265 million primarily driven by strong income from financing assets. This is clearly reflected in the Net Operating Revenue which grew by 11% YoY to reach to AED 5,580 million compared to AED 5,039 million last year.

Pre-impairment profit increased by 12% YoY reaching to AED 4,109 million compared to AED 3,684 million. Impairment charges reached AED 959 million, marginally up 1.2% YoY. However, 2Q 2023 charges of AED 463 million, were down 7% QoQ and 13% YoY.

Operating expenses amounted to AED 1,471 million during 1H 2023 vs AED 1,355 million in 1H 2022, exhibiting 8.5% YoY increase. The bank’s growth plans are well underway including continued enhancements on digital and transactional banking and further improvements on the customer experience journey. Following higher revenue growth and controlled cost growth, cost income ratio strengthened to 26.4%, down 50 bps YoY.

As a result, the bank’s Group Net Profit witnessed a strong increase of 15% YoY to reach AED 3,111 million (the highest in the bank’s history for the period under consideration) vs AED 2,700 million in 1H 2022. Q2 2023 net profit registered AED1,605 million up 6.6% QoQ and 18% YoY.

Net profit margin increased to 3.2% (+40bps YoY) with ROA and ROTE at a healthy 2.1% and 18.2% up by 10 bps and 120 bps YTD respectively.

Balance Sheet Trends

Net financing & Sukuk investments stood at AED 251 billion, up 5.3% YTD from AED 238 billion in FY 2022. DIB’s net financing assets were up by 2% YTD while the Sukuk investments portfolio, another key focus of the bank, expanded by nearly 18% YTD to reach to AED 61 billion.

DIB witnessed healthy overall YoY growth in gross new financing and sukuk in 1H 2023 amounting to nearly AED 45 billion, up 36% compared to AED 33 billion in 1H 2022. Gross corporate financing origination of nearly AED 21 billion (+ 23% YoY) driven mainly by large corporates, while new bookings from consumer financing accounted for AED 10 billion (+19% YoY), continued to exhibit DIB’s competence in deploying financing assets across all segments despite the ongoing market volatilities. Routine repayments of AED 13 billion and AED 8 billion from the corporate and consumer segments respectively kept flowing in given the elevated rate environment. Additionally, excess liquidity in the market led to early settlements from corporates of AED 6 billion. Despite this, net movement in the financing book led to a positive AED 3.5 billion in 1H 2023.

Customer deposits stood at AED 211 billion as of 1H 2023 up by 6% YTD on the back of a 5% increase in corporate deposits and an 8% increase in retail deposits. CASA now stands at AED 81 billion, comprising 39% of deposits. However, on a QoQ basis CASA showed an improvement by AED 1.5 billion. Migration to wakala deposits continued during the period due to the current global rate scenario. This is reflected through an increase in the wakala structure (investment deposits) which is up 16% YTD comprising a higher share of 61% of total deposits versus 56% in YE 2022. Liquidity coverage ratio (LCR) at 159%, up from 150% FY 2022, remains above regulatory requirement, depicting strong liquidity position.

Non-performing financing (NPF) ratio improved to 6.35%, down 11 bps compared YE 2022. Recoveries from NMC and NOOR POCI are ongoing which resulted in a decline of 10% in their NPF accounts. Additionally, coverage ratio on both accounts increased. For NMC coverage increased by 300 bps YTD to 77% and by 800 bps to 36% for the NOOR POCI account. Finally, core DIB NPF account witnessed a 1.2% uptick on a YTD basis to AED 10.9 billion well covered at 84%.

Stage 2 financing increased by 17% YTD to AED 18 billion due to normal flow between stages. On the other hand, Stage 3 coverage accordingly improved to 62.9%, (+170 bps) from FY2022 on the back of a concerted effort on recoveries.

Cash coverage ratio improved to 81% (+300 bps YTD, +700 bps vs 1H 2022) and overall coverage including collateral at 113% (+300 bps YTD and 1,000 bps vs 1H 2022) underpinning DIB’s commitment to enhancing its coverage ratio. Cost of risk on gross financing assets stood at 74 bps compared to 84 bps for the year 2022, an improvement of 10 bps YTD.

Capital ratios continue to remain strong with CAR now at 17.9% (up 30 bps YTD) and CET 1 ratio at 13.4% (up 50 bps YTD), both well above the regulatory requirement.

Business Performance (1H 2023)

Consumer Banking portfolio stood at AED 54 billion up 4% from AED 52 billion in FY2022. The portfolio’s total new underwriting of AED 10 billion during the period increased from AED 8.6 billion in 1H2022. In this, all consumer segments witnessed strong growth particularly auto finance which featured a 30% jump YoY and Personal Finance up 15% YoY in gross new underwriting. The business generated AED 2.4 billion in revenues during the year up a hefty 26% YoY from AED 2 billion during 1H 2022. Blended yield on consumer financing grew by 87 bps YoY to reach to 6.6%. Separately, on the funding side, consumer deposits witnessed an 8% increase YTD to AED 85 billion as investment deposits gained traction from customers while CASA remained steady YTD at AED 49 billion.

Corporate banking portfolio now stands at AED 136 billion up 1.5% YTD driven by automobile, financial institution and the utilities sectors. Gross new wholesale lending for 1H 2023 registered AED 21 billion up 23% YoY, while repayments and early settlements came in at AED 19.5 billion. Revenues featured double digit growth reaching AED 2.3 billion, up 39% YoY compared to AED 1.6 billion in 1H 2022. Yield on corporate financing portfolio expanded by 324 bps YoY to 6.21% compared to 2.97%. Separately on the funding side, corporate deposits increased by 5% YTD while CASA was impacted as large corporate rotate their deposits into investment higher yielding accounts.

Key Business Highlights (2Q 2023)

- DIB introduced an all-digital way of banking with ‘alt’- a comprehensive digital banking solution that integrates DIB’s extensive range of digital offerings and capabilities into one platform, providing customers with a seamless and hassle-free banking experience. The platform brings together more than 135 digital services via the DIB Mobile App, Online Banking, WhatsApp, and ATMs. This one-stop-shop for all banking needs enables customers to open a bank account in minutes, apply for personal finance or credit cards, remitting money locally or internationally, making payments, and much more. It has been designed to simplify banking processes and enhance convenience for customers across various touchpoints. By harnessing the power of advance technology, DIB ‘alt’ ensures an easy-going and efficient banking experience.

- As an organization that lives by its ICARE Values and aiming to provide further inclusive and productive environment, DIB announced the opening of AL AMANAH Parent Child Care Zone in Al Nahda Building to support its staff with work life balance and parenting in the workplace.

- The launch of “Premium Service”. The bank’s Call Center Unit launched the “Premium Service for Aayan & Wajaha Customers” – wherein a service team dedicated at offering the very best across customer service and experiences. The Premium Service is an initiative aligned to the bank’s strategic vision of becoming a stronger customer-centric organization, making our customers’ journey with the bank more rewarding and enriching one. Customers will be connected to the agents in a much shorter time period, thereby potentially resulting in faster resolutions.

- Tesla Event at GDRFA (General Directorate of Residency and Foreigners Affairs – Dubai). As part of DIB’s mission of being in sync with the global drive towards sustainability, DIB Auto Finance organized sales events in partnership with Tesla. The events were a great success as visitors and staff got the opportunity to experience TESLA Electric Vehicles and customers expressed their interest in DIB’s Evolve Auto Finance during the event.

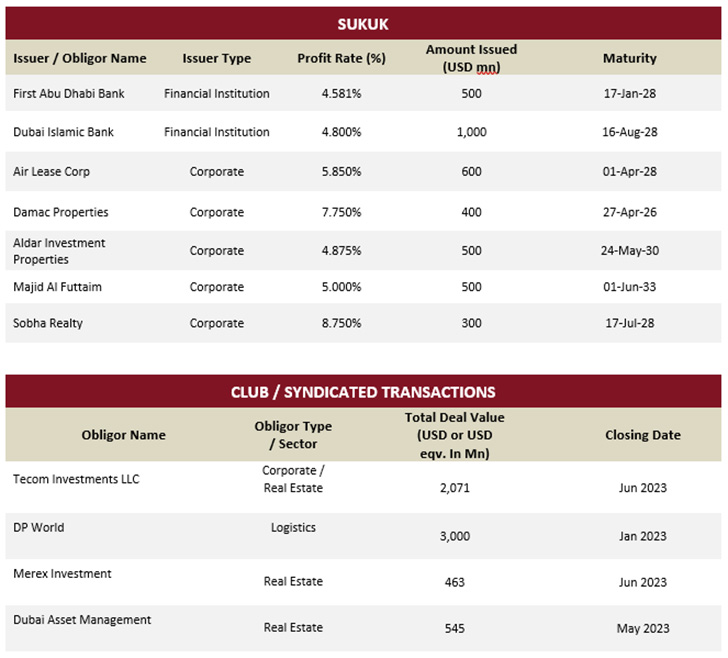

DCM and Syndication Deals (2023 YTD)

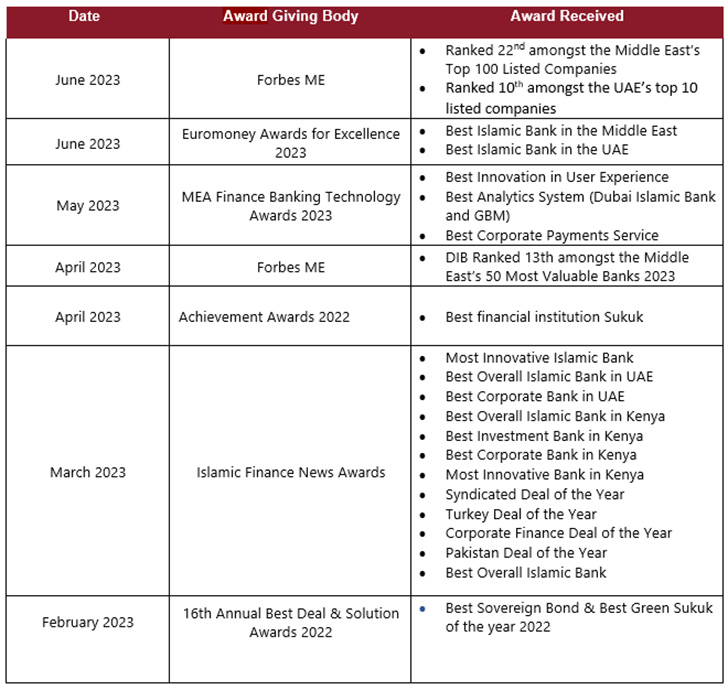

Awards List (2023 YTD)