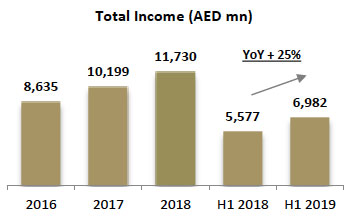

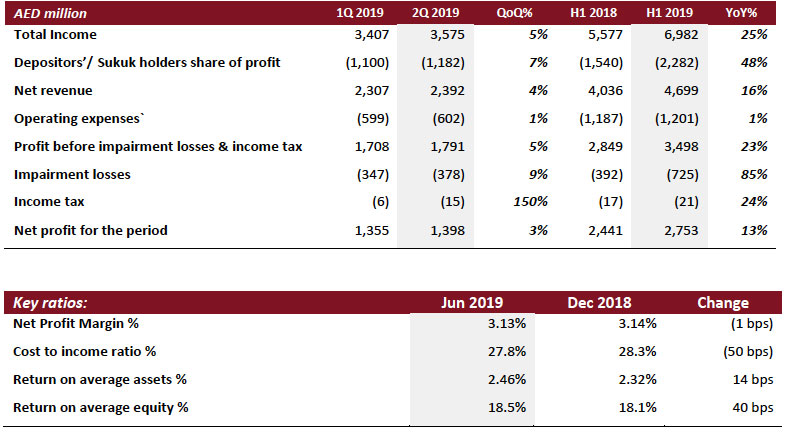

- Total income reaches AED 7.0 billion, growing by 25% YoY.

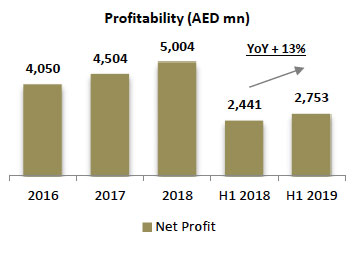

- Net Profit increases to AED 2.7 billion, up by 13% YoY.

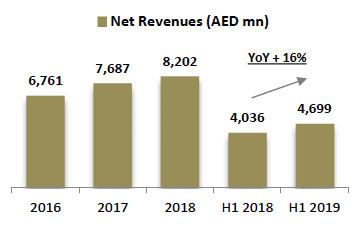

- Net Operating Revenue rose by 16% YoY to AED 4.7 billion.

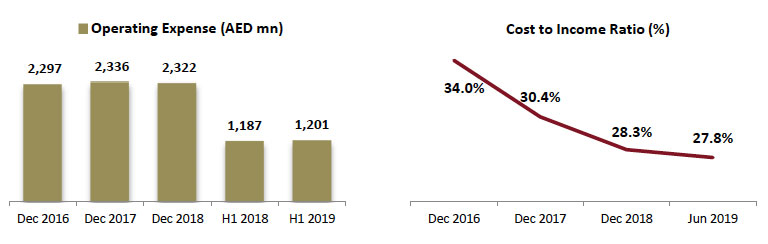

- Cost to Income ratio improves to 27.8%

Dubai Islamic Bank (DFM: DIB), the largest Islamic bank in the UAE, today announced its results for the period ending June 30, 2019.

H1 2019 Highlights:

Consistent rise in profitability (H1’ 19 vs H1’ 18)

- Group Net Profit increased to AED 2,753 million, up 13% compared to AED 2,441 million.

- Total Income increased to AED 6,982 million, up by 25% compared to AED 5,577 million.

- Net Operating Revenue grew to AED 4,699 million, up 16% compared to AED 4,036 million.

- Operating expenses stable at AED 1,201 million vs AED 1,187 million in H1 2018.

- Net operating profit before impairment charges grew by 23% to AED 3,498 million.

- Cost to income ratio continues to improve at 27.8% compared to 28.3% at the end of 2018.

- Net Profit Margin at 3.13% in line with guidance for the year.

Employing strength of balance sheet on growing core businesses:

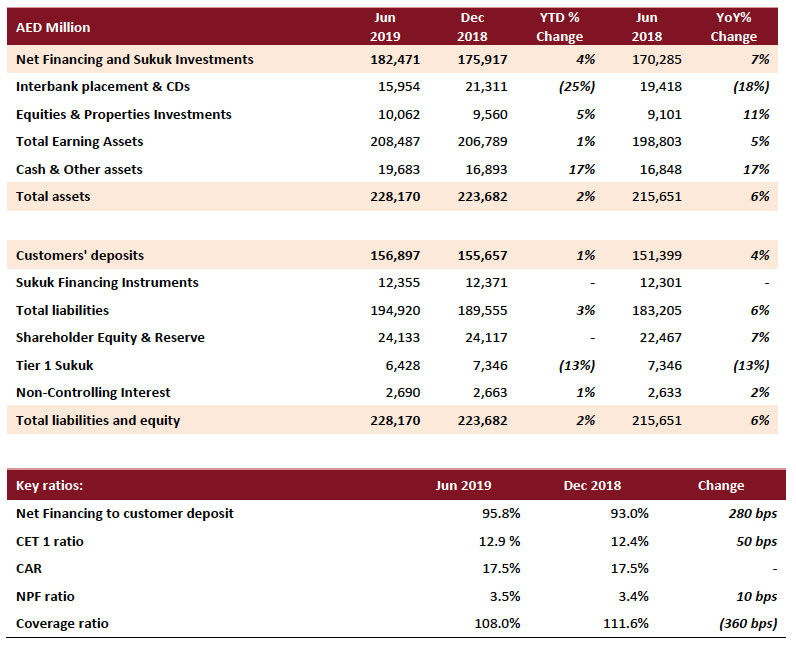

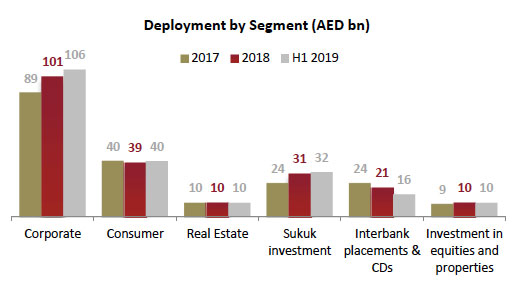

- Net Financing & Sukuk investments rose to AED 182.5 billion up by 3.7%, compared to AED 175.9 billion at the end of 2018.

- Total Assets stood at AED 228.2 billion, up by 2.0%, versus AED 223.7 billion at the end of 2018.

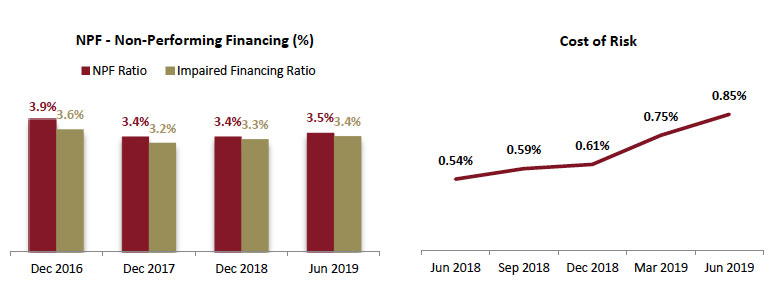

Stable asset quality:

- NPF ratio stable at 3.5% with cash coverage ratio is at 108%.

- Overall coverage, including collateral at discounted value, stands at 140%.

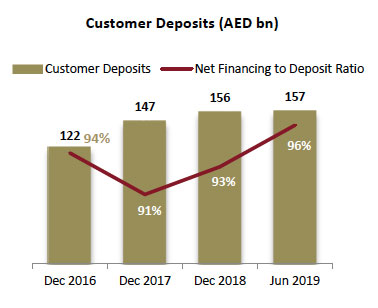

Strong Liquidity and Funding position:

- Customer deposits increased to AED 156.9 billion from AED 155.7 billion in end of 2018.

- CASA deposit increased by 6% year to date to reach at AED 57.2 billion as of H1 2019.

- Financing to deposit ratio stood at 96%.

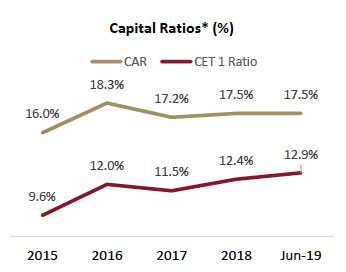

Well capitalized to support business growth :

- Capital adequacy ratio is at 17.5%, as against 13.50% minimum required.

- CET 1 is at 12.9%, as against minimum required of 10.00%, providing significant room for growth under the new Basel III regime.

- ROA increased to 2.46% and ROE at 18.5%, both in line with guidance.

Management’s comments for the period ending June 30, 2019:

His Excellency Mohammed Ibrahim Al Shaibani, Director-General of His Highness The Ruler’s Court of Dubai and Chairman of Dubai Islamic Bank, said:

- With the constant evolution of an efficient and robust governance model and progressive approach to infrastructure development, the UAE now ranks amongst the leading global markets for business and economic competitiveness.

- The opening up of key economic sectors for foreign ownership will lead to increased investment and higher employment opportunities for the domestic economy as the country retains its position as an attractive place to do business.

- With double digit rise in profitability, the bank remains in a strong position to capture opportunities in the market whilst delivering robust growth and returns for all stakeholders.

Dubai Islamic Bank Managing Director, Abdulla Al Hamli, said:

- We continue to sustain the growth of our balance sheet evidenced by the consistent increasing market share of DIB in the industry over the past few years.

- The progress on digital ambitions continues with the launch of significantly enhanced products and services to the modern customer leading to a more personalized and secured banking journey that can be experienced anytime and anywhere.

Dubai Islamic Bank Group Chief Executive Officer, Dr. Adnan Chilwan, said:

- We have built a dynamic, flexible and adaptive organization that can sustain business and growth in any kind of economic environment.

- Whilst we continue to show robust balance sheet growth, profitability is and will always remain the key area of focus for DIB, evidenced by ROA at 2.46% and ROE at 18.5%, which is amongst the strongest in the market.

- Fostering a culture of growth in the organization has been a key factor in the successful contribution from all businesses across wholesale and consumer, both now being ably supported by digital enhancements that have significantly strengthened our delivery and servicing capabilities across the entire breadth of our diverse customers base.

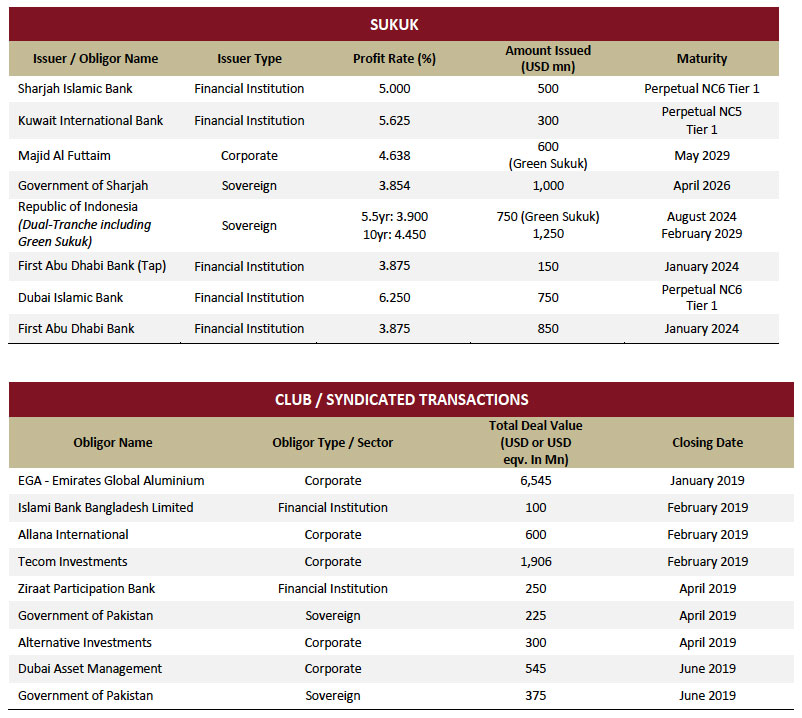

- With more than USD $ 6 billion of sukuk issuances and nearly USD $ 11 billion in syndicated deals since the start of the year, the bank’s franchise continue to dominate the corporates and sovereigns business in the international Islamic capital market space.

- The discipline in managing our costs and focusing on efficiency building has yielded very strong results with net profit growing by 13% YoY to reach AED 2.7 bn. Our cost to income is now at a historical low of 27.8%.

- Our improving asset quality over the years is a result of the bank’s prudent and conservative approach to underwriting with quality credit building rather than balance sheet expansion at the core of the growth strategy.

Financial Review

Income Statement highlights:

Total Income

Total income for the period ended 30 June 2019 reached AED 6,982 million, up 25% YoY. The strong income growth can be attributed to robust growth in income from Islamic financing and investing assets growing at 19% as well as income from investments in Islamic sukuk which grew at 33%.

Net revenue

Net revenue for the period ended 30 June 2019 amounted to AED 4,699 million, an increase of 16% compared with AED 4,036 million in H1 2018. The bank’s continued efforts to diversify into key sectors of the domestic economy have supported the continued core revenue growth over the past few years.

Operating Expenses

Operating expenses for the period ended 30 June 2019 remained broadly stable at AED 1,201 million compared to AED 1,187 million in H1 2018. Cost to income ratio continuous to improve now at 27.8% compared to 28.3% at the end of 2018. The bank’s continued investments in digital capabilities and technology have enabled the bank to unlock significant operational efficiencies within its network.

Net Profit

Net profit grew strongly by 13% to AED 2,753 million for the period ended 30 June 2019 from AED 2,441 million in H1 2018. Strong income growth from the bank’s key businesses coupled with a well-disciplined cost management have supported the robust growth in net profit for the period.

Statement of financial position highlights

Financing and Sukuk portfolio

Net financing & sukuk investments increased to AED 182.5 billion for the period ended 30 June 2019 from AED 175.9 billion at the end of 2018, an increase of over 3.7%, primarily driven by continued healthy core business growth and focus on diversification throughout the past few years. Corporate banking financing assets currently stand at AED 106 billion whilst the consumer financing assets stood at AED 40 billion, the latter supported by new financing of around AED 7.0 billion. Commercial real estate concentration managed within guidance at around 20%.

Asset Quality

For the period ended 30 Jun 2019, non-performing financing ratio and impaired financing ratio stood at 3.5% and 3.4% respectively. Cash coverage stood at 108% and overall coverage ratio including collateral at discounted value reached 140% with cost of risk (on gross financing assets) at 85 bps.

Customer Deposits

Customer deposits for the period ended 30 June 2019 reached to AED 157 billion from AED 156 billion in end of 2018. CASA deposit grew by 6% year to date to reach AED 57 billion and net financing to deposit ratio stood at 96%. The bank continues its strong focus in enhancing its CASA base through pushing on salary accounts and cash management products.

Capital Adequacy

Capital adequacy ratios remained robust with overall CAR and CET 1 ratio for the period ended 30 June 2019 standing at 17.5%, (against minimum CAR requirement of 13.5%), and 12.9%, (against minimum CET1 requirement of 10%), respectively. DIB has been designated a Domestic Systemically Important Bank (D-SIB) by the regulator, which signifies the importance of the franchise to the financial sector in the country.

* Above graph reflects amended prior year values under the new Basel III regime

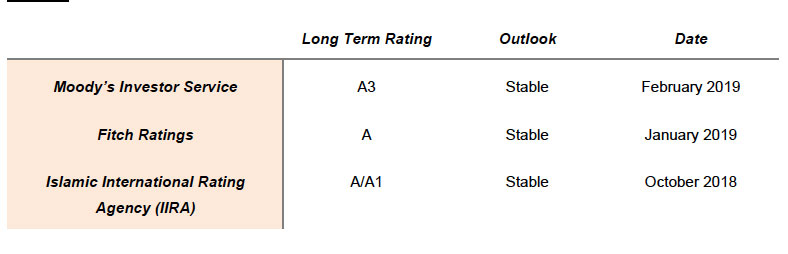

Ratings

- February 2019 – Moody’s publishes DIB credit opinion update re affirming the bank’s long term issuer rating scale ‘A3’ carrying a ‘Stable’ outlook supported by healthy profitability, stable asset quality with sound capital and liquidity.

- January 2019 - Fitch Ratings has re-affirmed Dubai Islamic Bank (DIB) Long-Term Issuer Default Rating (IDR) at ‘A’ with a Stable Outlook and Viability Rating (VR) at ‘bb+’ reflecting strong domestic franchise, healthy profitability and sound liquidity.

- October 2018 – Islamic International Rating Agency (IIRA) has reaffirmed ratings on Dubai Islamic Bank with international scale ratings of A/A1. The strong ratings are driven by consistent improvement of asset quality indicators over time, continued growth in business assets and strong cost controls leading to robust profitability.

Q2 2019 - Key business highlights

- During the 1st half of 2019, DIB continuous its dominance in the capital markets space both domestic and internationally by taking part in more than USD $ 6 billion of sukuk issuances and nearly USD 11 billion in syndicated deals for sovereigns, financial institutions and large corporates. As a major arranger and bookrunner, these deals have propelled the bank to retain its leading position across the Bloomberg capital markets league tables in the first half of 2019. In addition, the bank has also increased its efforts to support sustainable development initiatives by being part of the highly successful first corporate green sukuk in the region and marking the second green financing Sukuk issued by a large sovereign in Asia.

- The bank continues to be a leading provider of cash management services in the banking sector following implementation of payment mandates with the Department of Finance (DOF) and Government of Ajman. The integrated and innovative DIB digital H2H “Host-to-Host” payment solution already has an established track record having been operational since 2015. In addition, DIB Cash Management also successfully launched the ‘VASCO DigiPass’ – a smart highly secured and portable digital app, for ePayments authorization for corporate clientele enabling them to undertake services and secured payments through the app.

- During the quarter, customer journeys on self-service platforms (mobile and internet banking) were launched for pre-approved credit cards and personal finance. Such customers are now able to complete end-to-end journeys, from initiation to card issuance or funds disbursal, without the need to engage with sales staff. Furthermore, this will significantly reduce the cost of acquisition for such product offerings.

YTD 2019 Syndications and Deals

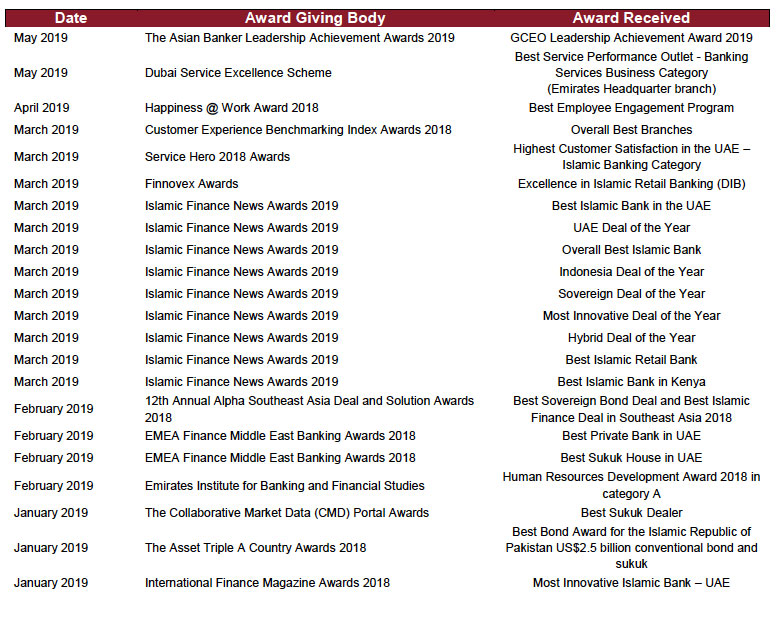

Industry Awards (Year to Date 2019)