DIB Net Profit reaches AED 3.301 billion as balance sheet crosses AED 200 billion:

- Group net profits up by 10% YoY to reach to AED 3.301 billion.

- Financing assets grew by 14% YTD to AED 131.3 billion.

- Deposits increased by 17% YTD to AED 143.5 billion.

Dubai Islamic Bank (DFM: DIB), the first Islamic bank in the world and the largest Islamic bank in the UAE by total assets, today announced its results for the period ended September 30, 2017.

9M 2017 Results Highlights:

Sustained profitability and growth on the back of robust Net Income Margin (NIMs) and low operating expenses:

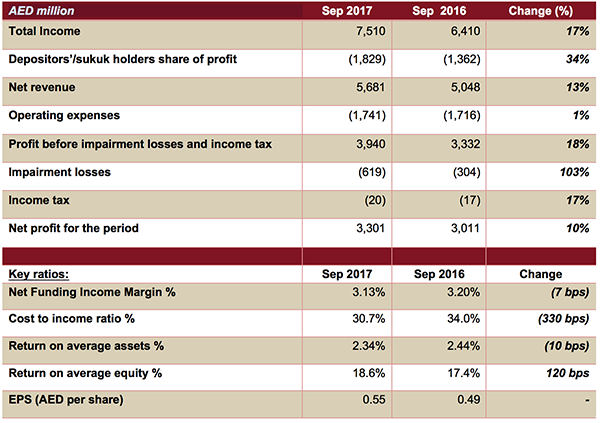

- Group Net Profit increased to AED 3,301 million, up 10% compared with AED 3,011 million for the same period in 2016.

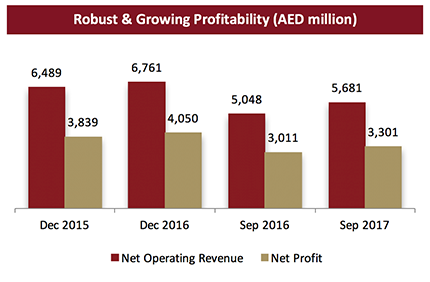

- Total income increased to AED 7,510 million, up 17% compared with AED 6,410 million for the same period in 2016.

- Net Operating Revenue increased to AED 5,681 million, up 13% compared with AED 5,048 million for the same period in 2016.

- Efficient and proactive cost management led to operating expenses remaining nearly flat at AED 1,741 million compared to AED 1,716 million for the same period in 2016.

- Net operating income before impairment charges grew by 18% to AED 3,940 million compared to AED 3,332 million for the same period in 2016.

- Cost of credit risk reduced to 63 bps compared to 81 bps for the same period in 2016.

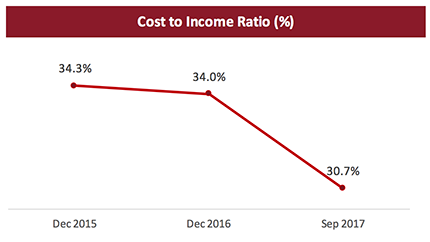

- Cost to income ratio reduced to 30.7% compared with 34.0% at the end of 2016.

Asset growth remains robust across all core businesses

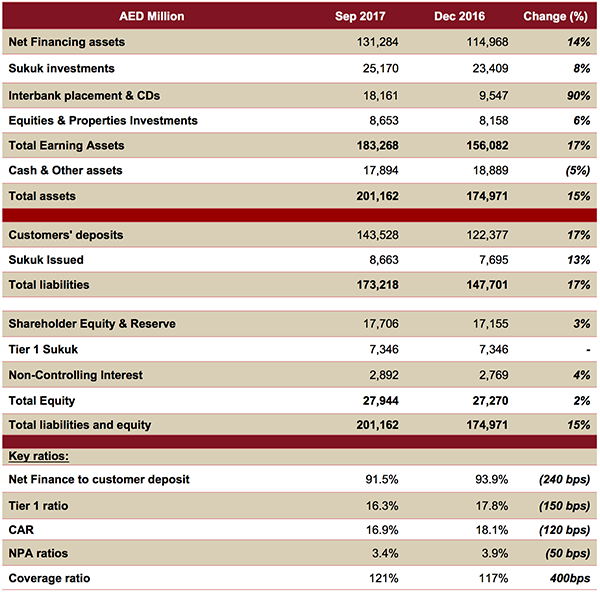

- Net financing assets rose to AED 131.3 billion, up by 14%, compared to AED 115.0 billion at the end of 2016.

- Sukuk investments increased to AED 25.2 billion, a growth of 8%, compared to AED 23.4 billion at the end of 2016.

- Total Assets stood at AED 201.2 billion, an increase of 15%, compared to AED 175.0 billion at the end of 2016.

Asset quality trends remain positive, a direct consequence of robust underwriting and solid risk management practices

- NPA ratio continues its downward trajectory improving to 3.4%, compared to 3.9% at the end of 2016.

- Provision coverage ratio improved to 121%, compared to 117% at the end of 2016.

- Overall coverage including collateral at discounted value now stands at 162%, compared to 158% at the end of 2016.

Strong liquidity continues to support asset growth

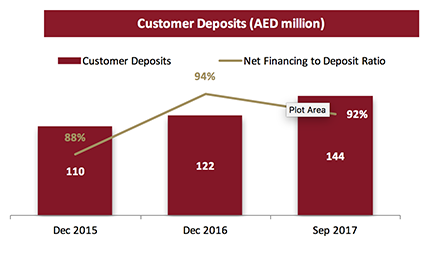

- Customer deposits stood at AED 143.5 billion compared to AED 122.4 billion at the end of 2016, up by 17%.

- CASA deposits increased by nearly 7% to AED 50.9 billion from AED 47.4 billion as at end of 2016 leading to a robust 35% constitution of the total deposit base.

- Financing to deposit ratio stood at 92%, indicating a push towards efficiency and margin protection.

- Focus on diversification and securing long term funding saw another successful senior sukuk issuance of USD 1 billion during Q1 2017.

Robust Capitalization

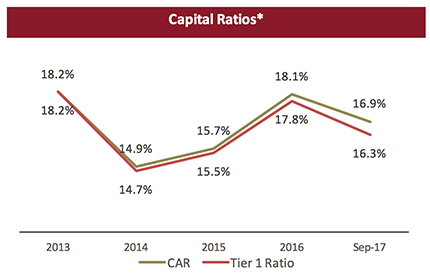

- Capital adequacy ratio remained strong at 16.9%, as against 12% minimum required.

- Tier 1 CAR stood at 16.3% under Basel II, against minimum requirement of 8%.

Shareholders’ return remains robust – in line with guidance for the year

- Earnings per share stood at AED 0.55 as at Q3 2017.

- Return on equity stood at 18.6% as at Q3 2017.

- Return on assets steady at 2.34% as at Q3 2017.

Management’s comments on the financial performance for period ended September 30, 2017:

His Excellency Mohammed Ibrahim Al Shaibani, Director-General of His Highness The Ruler’s Court of Dubai and Chairman of Dubai Islamic Bank, said:

- The recovery of international oil prices and the stability witnessed in the recent past will be a major source of support in the area of funding and liquidity for the banking sector.

- With the solidity and resilience displayed by UAE’s financial market, credit growth is expected to more than double to 5% in 2018, spurred by the government’s unabated progress on infrastructure development in line with its economic aspirations.

- DIB continues to remain at the forefront of the industry with solid earnings growth as net profit increased by 10% YoY, primarily driven by the bank’s persistent efforts in maximizing its share of wallet across a diverse array of sectors and

segments.

Dubai Islamic Bank Managing Director, Abdulla Al Hamli, said:

- The bank has given another remarkable performance this quarter with total income growing by 17% YoY as DIB continues to outpace the sector growth.

- The progress we have made in implementing our growth aspirations has led to the bank strengthening its market share with both the financing book and the deposit base growing by mid to high double digits in the first nine months of 2017.

- With the rapidly changing digital space, we will continue to expand on our technological capabilities to ensure that we remain at the forefront of the FINTECH revolution, and our customers get the best and most convenient product and services at all

times.

Dubai Islamic Bank Group Chief Executive Officer, Dr. Adnan Chilwan, said:

- Crossing the landmark of AED 200 bln in total assets is another momentous milestone in our incredible growth journey over the last four years. This market beating performance clearly demonstrates the strength of the franchise and the potential the

organization has to continue to defy the trend despite the challenges thrown by the global economic environment.

- The recent move by the rating agencies with positive impacts on long term as well as standalone ratings is a clear affirmation of the fact that the 14% growth in the financing assets so far this year and the tremendous performance in preceding years

has not come at the expense of asset quality or underwriting standards. A testament to the tight and stringent risk management practices in DIB, these announcements by the two international rating agencies should provide a strong sense of comfort

to our growing global investor community.

- With a sector share of around 8%, DIB today, has the required scale, positioning and the financial strength to continue to deliver above-market performance.

- Bolstering the international presence will see us engage actively in the existing core markets as we expand our focus geographies to now include South East Asia, East Africa and Far East Asia.

- The progress so far has been backed by a thorough and solid strategic agenda built on a model of preemptive capacity creation. With ample liquidity and robust capitalization serving as the backbone to DIB’s growth objectives, the bank is in

a strong position to accelerate its plans to expand its franchise locally and internationally and ensure that we continue to deliver even more comprehensive, creative and complete solutions to all our customers in the markets we operate.

Financial Review

Income Statement highlights:

Total Income

Profitability remained strong with total income for the period ended September 30, 2017 increasing to AED 7,510 million from AED 6,410 million for the same period in 2016. The 17% rise is driven primarily by sustained growth in all core businesses with

income from Islamic financing and investing assets increasing by 19% to AED 5,722 million compared to AED 4,813 million for the same period in 2016.

Net revenue

Net revenue for the period ended September 30, 2017 amounted to AED 5,681 million, an increase of 13% compared with AED 5,048 million in the same period of 2016. The increase is attributed to strong growth in the financing book as the bank continues to

enhance its share of wallet across all key economic sectors.

Operating expenses

Operating expenses were held nearly flat to AED 1,741 million for the period ended September 30, 2017 compared to AED 1,716 million in the same period in 2016, primarily due to efficient cost management. This led to cost to income ratio improving to 30.7%

compared to 34.0% at the end of 2016.

Profit for the period

Net profit for the period ended September 30, 2017, rose to AED 3,301 million from AED 3,011 million in the same period in 2016, an increase by 10% emanating from a combination of robust core business growth and effective and efficient cost management.

Statement of financial position highlights:

Financing portfolio

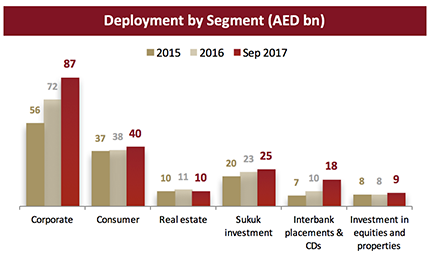

Net financing assets grew to AED 131.3 billion for the period ended September 30, 2017 from AED 114.9 billion as of end of 2016, an increase of 14% driven primarily by the continued growth of core businesses. Corporate banking financing assets grew by

21% to AED 87 billion whilst consumer business grew by 4% to AED 40 billion. Commercial real estate concentration contained at around 18% and in line with targeted guidance numbers.

Asset Quality

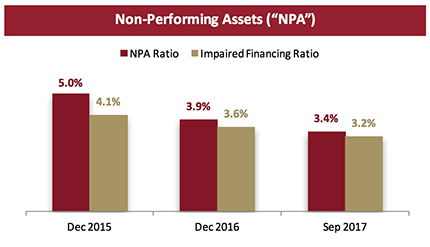

Non-performing assets have shown a consistent decline with NPA ratio improving to 3.4% for the period ended September 30, 2017, compared with 3.9% at the end of 2016. Impaired financing ratio stood at 3.2% for the period ended September 30, 2017 from

3.6% at the end of 2016. Consequently, as buildup of provision continuous driven primarily by collective provisioning, cash coverage stood at 121% for the period ended September 30, 2017 compared with 117% at the end of 2016. Overall coverage ratio

including collateral at discounted value stood at 162% compared to 158% at the end of 2016.

Sukuk Investments

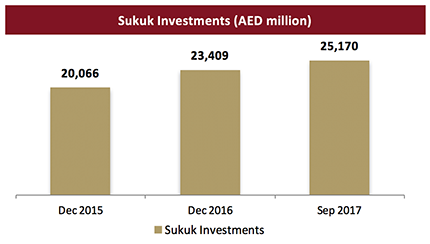

Sukuk investments increased by 8% to AED 25.2 billion for the period ended September 30, 2017 from AED 23.4 billion at the end of 2016. This high yielding portfolio, primarily listed and based out of UAE, consists of sovereigns and other top tier names

many of which are rated.

Customer Deposits

Early capacity creation, with liquidity mobilization continues to spur growth. Customer deposits for the period ended September 30, 2017 increased by 17% to AED 143.5 billion from AED 122.4 billion as at end of 2016. CASA component stood at AED 50.9 billion

as of September 30, 2017 compared with AED 47.4 billion as at end of 2016 showing consistent rise in low cost deposits. Financing to deposit ratio of 92% as of September 30, 2017 indicates one of the strongest liquidity position.

Capital Adequacy

Capital adequacy ratio remained robust at 16.9% as of September 30, 2017, whilst T1 ratio stood at 16.3%; both ratios are well above regulatory requirement in the current Basel II regime.

* Regulatory Capital Requirements CAR at 12% and Tier 1 at 8%

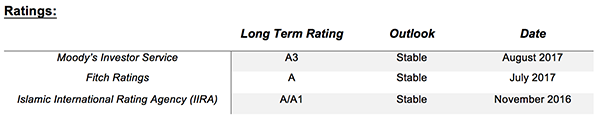

- Aug 2017 – Moody’s upgrades DIBs long-term issuer ratings to ‘A3’ from Bass1; outlook ‘Stable’.

- Jul 2017 - Fitch has upgraded the bank’s standalone VR to ‘bb+’' from ‘bb’ citing robust and continuous improvement across the major key metrics including profitability and asset quality.

- The moves clearly point towards not just the financial strength of the existing franchise but the confidence the stakeholders have in its ability to sustain robust profitability in the foreseeable future.

Key business highlights for the 3rd quarter of 2017:

- Moody’s Investors Service has upgraded Dubai Islamic Bank’s (DIB) local and foreign currency long-term issuer ratings to ‘A3’ from ‘Baa1’ and also upgraded is baseline credit assessment (BCA) and adjusted BCA to

‘ba2’ from ‘ba3’. This upgrade reflects the bank’s significantly improved asset quality and provisioning coverage; solid and improving profitability and sound capitalization and liquidity.

- Fitch Ratings also upgraded the viability (standalone) rating of the bank citing a stronger positioning across all key metrics.

- Corporate Banking has launched its "ICCS-Corporates" Image Cheque Clearing System. The online, smart system allows the instant scanning of customers' cheques and direct deposit of funds into customers' accounts the same day. The service, fully supported

by the UAE Central Bank, is aimed at improving the customer experience by providing quicker access to funds and real-time account & cheque status updates.

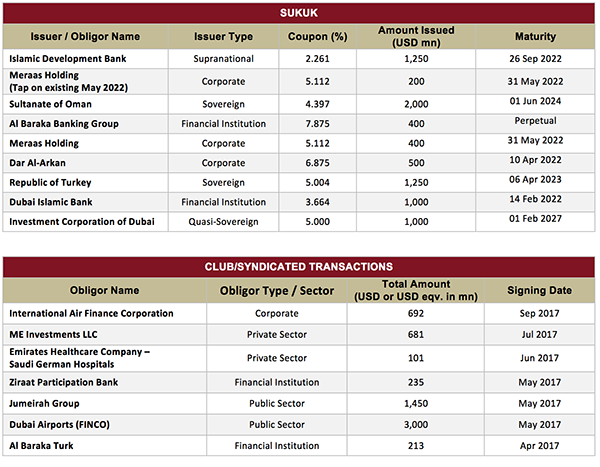

- Year to Date key deals

Year to Date 2017 Awards: