Net profit up by 7% to over AED 3 billion

Dubai Islamic Bank (DFM: DIB), the first Islamic bank in the world and the largest Islamic bank in the UAE by total assets, today announced its results for the period ended September 30, 2016.

Year to Date Results Highlights:

Resilient performance amidst market volatilities:

Strong balance sheet growth

Asset quality continues to improve

Steady growth in customer deposits

Improved capital position post rights issue

Enhancing value for shareholders

Management’s comments on the financial performance of the financial period:

His Excellency Mohammed Ibrahim Al Shaibani, Director-General of His Highness The Ruler’s Court of Dubai and Chairman of Dubai Islamic Bank, said:

Despite somewhat difficult times for the global economy, the UAE economy and banking sector continues to remain resilient with healthy profitability and strong capitalization levels across the industry. Dubai’s economic diversification has placed the emirate in a robust position to actively pursue its long term goals, particularly in the field of Islamic finance and economy. DIB’s strategy remains aligned to the emirate’s agenda as the bank has, once again, come out with a stellar performance despite the challenging environment.

Dubai Islamic Bank Managing Director, Abdulla Al Hamli, said:

The bank’s year to date performance has been very encouraging on the back of the strategy we had embarked on in 2014. We are clearly positioning the bank strongly for future as we continues to progress steadily towards our strategic and financial aspirations. The sustained improvement in our asset quality throughout the last few years is a further testament to our continued discipline and proactive approach towards risk management. Our growth momentum remains solid driven by the expansion of our core business as we continue penetrate in existing and new sectors.

Dubai Islamic Bank Group Chief Executive Officer, Dr. Adnan Chilwan, said:

“Everyone talks of organizational agility today”, said Dr. Adnan Chilwan, GCEO, DIB. “We have to be nimble and quick to respond to the market volatilities which have been the only constant over the current times. Whilst being able to think on your feet is important, I am of the view that such capabilities and, consequently the associated flexibility, can be built into the DNA of the organization, and these then become the critical drivers in turbulent periods. DIB has, over the years, proven just that. We used all ingredients available to us – people, technology, expertise to name a few – and combined them to create this platform that sustained growth throughout the last three years when the market was definitely being viewed as challenging to say the least.

“Our balance sheet has grown by more than 50% in under three years which, given the global economic environment, is a remarkable feat”, he added. “In doing so we have nearly doubled our financing book, yet managed to maintain a strong liquidity position. Finally, we have kept the interest of all stakeholders in mind, so whilst the shareholder’s returns have been growing with rising profitability, the asset quality and capitalization remain strong and robust, a testament to both the quality of the financing book and the quality of risk management practices deployed within the bank. I look forward to another strong performance from DIB as we close 2016 and am confident of many more prosperous years ahead.”

Financial Review

Income Statement highlights:

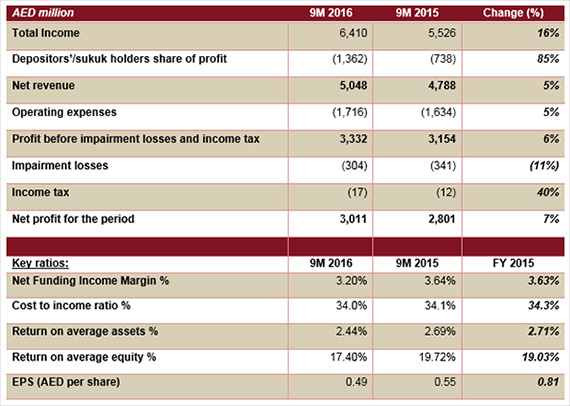

Total Income

Profitability remained strong despite challenging economic environment. Total income for the period ended September 30, 2016 increased to AED 6,410 million from AED 5,526 million for the same period in 2015, an increase of 16% driven primarily by continued growth in core businesses. Income from Islamic financing and investing transactions increased by 18% to AED 4,767 million from AED 4,043 million for the same period in 2015. Fees and commissions have increased by 15% to AED 1,119 million compared to AED 975 million for the same period in 2015.

Net revenue

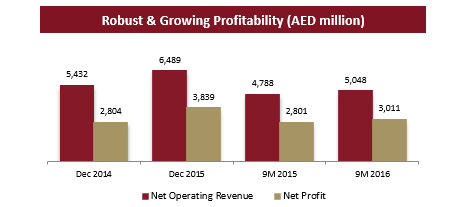

Net revenue for the period ended September 30, 2016 amounted to AED 5,048 million, an increase of 5% compared with AED 4,788 million in the same period of 2015. The increase is attributed to build up of core financing assets as well as growth in commissions and fees.

Operating expenses

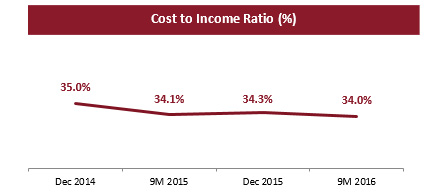

Operating expenses slightly increased by 5.0% to AED 1,716 million for the period ended September 30, 2016, from AED 1,634 million in the same period in 2015, primarily due to growth in business volumes. However, cost to income ratio remained stable at 34.0% compared to 34.1% for the same period in 2015, in line with guidance for the year.

Impairment losses

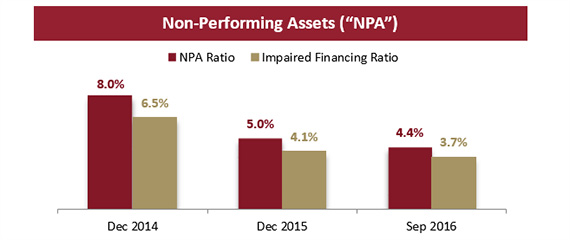

Impairment losses declined to AED 304 million compared with AED 341 million for the same period in 2015, an improvement of 11%. NPLs dropped by 60 bps within the first nine months to reach to 4.4%, showing continuous and constant improvement in asset quality.

Profit for the period

Net profit for the period ended September 30, 2016, rose to AED 3,011 million from AED 2,801 million in the same period in 2015, an increase by 7% depicting robust profitability growth despite slow economic environment.

Statement of financial position highlights:

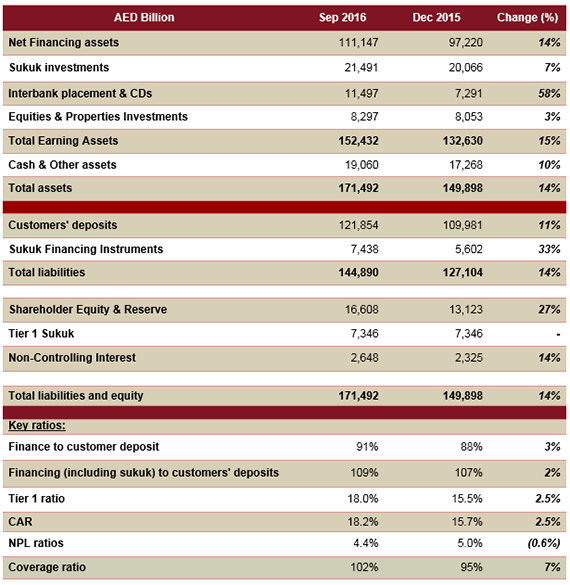

Financing portfolio

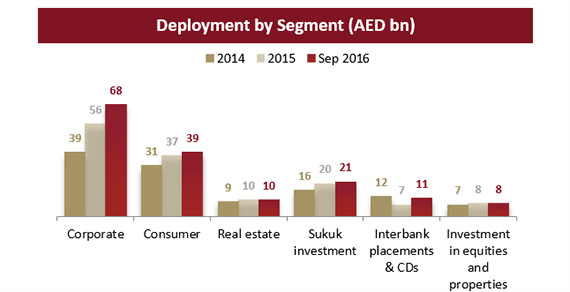

Net financing assets grew to AED 111.1 billion for the period ended September 30, 2016 from AED 97.2 billion as of end of 2015, an increase of 14% as the bank continued its penetration in various targeted sectors particularly on the wholesale side of the business. Corporate banking grew at 21% to AED 68 billion whilst consumer business grew by 5% to AED 39 billion.

Asset Quality

Non-performing assets have shown a consistent decline with NPL ratio improving to 4.4% for the period ended September 30, 2016, compared with 5.0% at the end of 2015. Impaired financing ratio also improved to 3.7% for the period ended September 30, 2016 from 4.1% at the end of 2015. The improving NPLs and impaired ratio is primarily driven by recoveries in legacy portfolio as well as continuous growth in the quality asset book. With constant buildup of provisions, cash coverage improved to 102% compared with 95% at end of 2015. Overall coverage ratio stood at 152% at the end of September 2016 compared to 147% at the end of December 2015.

Sukuk Investments

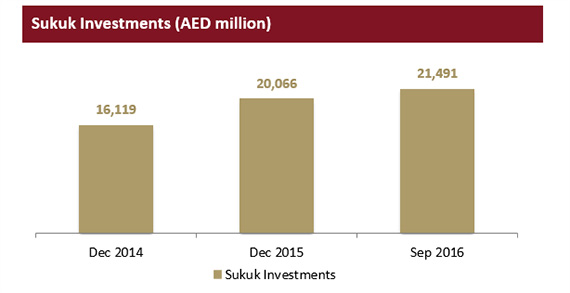

Sukuk investments increased by 7% for the period ended September 30, 2016 to AED 21.5 billion from AED 20.1 billion at end of 2015. The primarily dollar denominated portfolio consists of sovereigns and other top tier names many of which are rated.

Customer Deposits

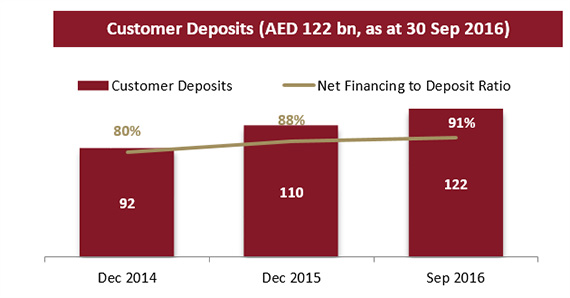

Customer deposits for the period ended September 30, 2016 increased by 11% to AED 122 billion from AED 110 billion as of end of 2015. CASA component stood at AED 48.2 billion compared with AED 44.6 billion in 2015. Investment deposits grew by 13% for the period ended September 30, 2016 to AED 73.6 billion from AED 65.4 billion as at end 2015. Financing to deposit ratio of 91% as of September 2016 denotes that the bank remains amongst the most liquid players in the market despite strong financing growth and challenging liquidity environment.

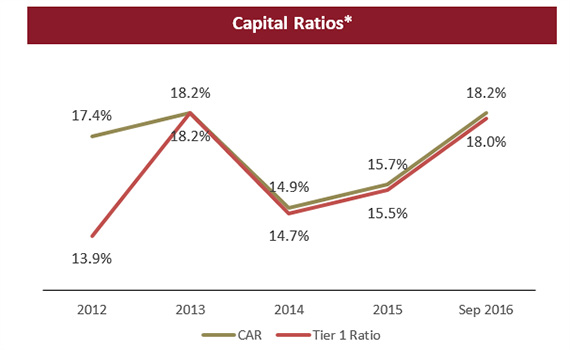

Capital and capital adequacy

Strong profitability along with the recent successful rights issue has led to overall CAR growing to 18.2%. This strong level of capitalization will be a major factor in supporting the future growth agenda.

* Regulatory Capital Requirements CAR at 12% and Tier 1 at 8%

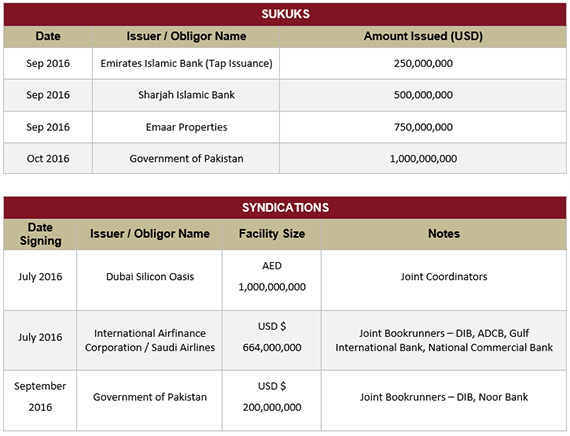

Key business highlights for the 3rd quarter of 2016:

Year to date 2016 Awards:

DIB Successfully Issues Debut Sustainability-Linked Financing Sukuk

DIB and HCLTech Forge Strategic AI Innovation Partnership