H1 2016 net profit up by 11% to over AED 2 billion

Dubai Islamic Bank (DFM: DIB), the first Islamic bank in the world and the largest Islamic bank in the UAE by total assets, today announced its 1st half results for the period ended June 30, 2016.

H1 2016 Results Highlights:

Resilient performance amidst market volatilities:

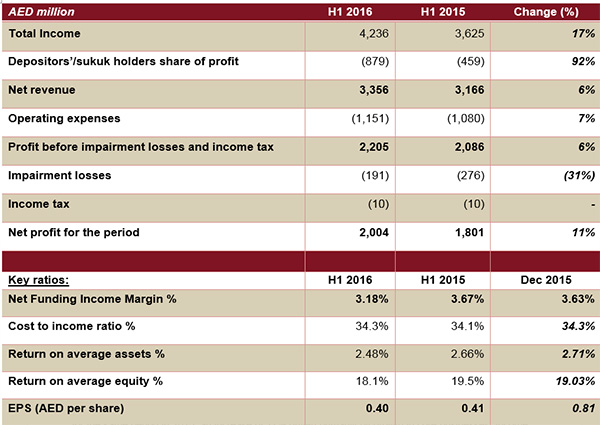

- Group Net Profit increased to AED 2,004 million, up 11% compared with AED 1,801 million for the same period in 2015.

- Total Income increased to AED 4,236 million, up 17% compared with AED 3,625 million for the same period in 2015.

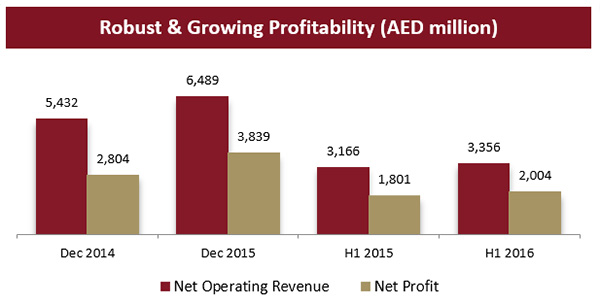

- Net Operating Revenue increased to AED 3,356 million, up 6% compared with AED 3,166 million for the same period in 2015.

- Impairment losses declined to AED 191 million compared with AED 276 million for the same period in 2015.

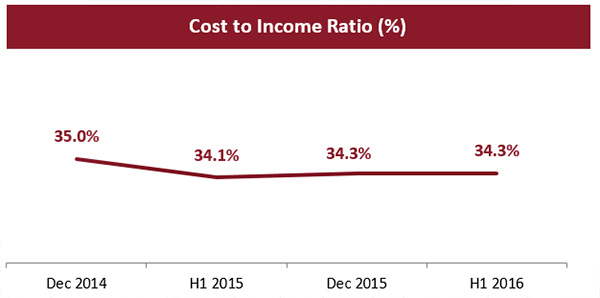

- Cost to income ratio remained stable at 34.3% compared with 34.1% for the same period in 2015, in line with guidance for the year.

Strong balance sheet driven by growth in core business activities

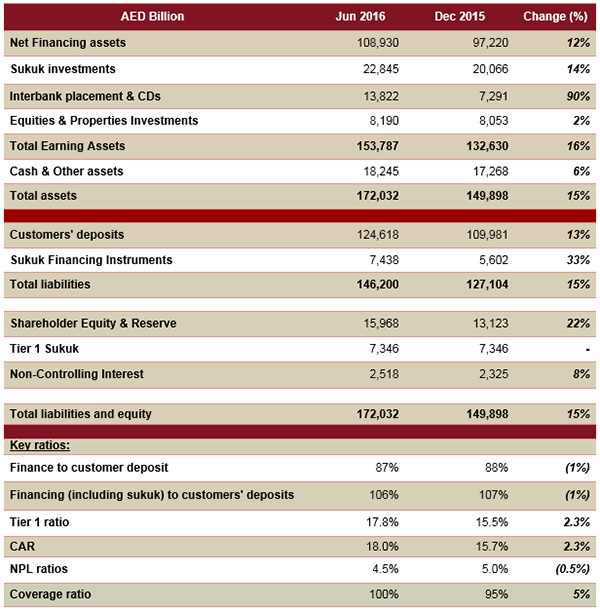

- Net financing assets at AED 108.9 billion up by 12%, compared to AED 97.2 billion at the end of 2015, in line with guidance for the year.

- Sukuk investments at AED 22.8 billion, an increase of 14%, compared to AED 20.1 billion at the end of 2015.

- Total Assets at AED 172 billion, an increase of 15%, compared to AED 149.9 billion at the end of 2015.

Improving asset quality

- NPLs on a consistent decline with NPL ratio improving to 4.5%, compared to 5.0% at the end of 2015.

- Provision coverage ratio improved to 100%, compared to 95% at the end of 2015. Overall coverage including collateral at discounted value now stands at 150%, compared to 147% at the end of 2015.

Steady growth in customer deposits

- Customer deposits at AED 125 billion compared to AED 110 billion at the end of 2015, up by more than 13%.

- CASA book enhance to 41.3% of total deposit base compared to 40.6% at the end of 2015, despite challenging liquidity environment.

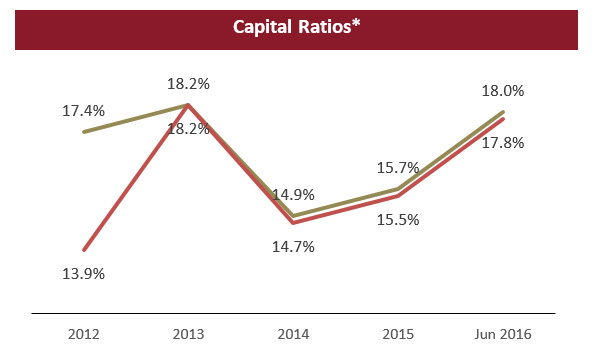

Maintaining strong capitalization ratios

- Capital adequacy ratio at 18.0% as of June 2016, as against 12% minimum required.

- Tier 1 CAR stood at 17.8% against minimum requirement of 8%.

- Financing to deposit ratio is at 87% highlighting significant liquidity.

Enhancing value for shareholders

- Earnings per share stood at AED 0.40 in 1H 2016.

- Return on assets is at 2.48% in 1H 2016, in line with guidance given for the year.

- Return on equity stood at 18.1% in 1H 2016, in line with guidance given for the year.

Management’s comments on the financial performance of the financial period:

His Excellency Mohammed Ibrahim Al Shaibani, Director-General of His Highness The Ruler’s Court of Dubai and Chairman of Dubai Islamic Bank, said:

- These continue to be challenging times with substantial economic impacts stemming from global events. The Brexit decision further added an air of uncertainty to the global economic scenario.

- DIB continues to impress with its performance as one the most attractive and profitable franchise in the country.

- The board and the management remain focused on effectively executing the growth strategy that not only achieves results in the short term but also builds capabilities and platform to sustain the same in the years to come.

Dubai Islamic Bank Managing Director, Abdulla Al Hamli, said:

- The bank has once again, delivered robust results during the first half of 2016 aligned with the UAE economy’s resilience to the commodity prices volatility.

- The bank’s recent capital increase via a rights issue was heavily oversubscribed denoting the strong shareholder interest in the franchise.

Dubai Islamic Bank Group Chief Executive Officer, Dr. Adnan Chilwan, said:

- DIB’s performance over the last two years, despite the current economic conditions, has been remarkable to say the least. Our growth guidance was well above the market and we have managed to beat those consistently.

- In a challenging and highly competitive liquidity landscape, we have shown the ability to generate not just a double digit deposit growth, but also growth in the low cost funding for the bank.

- Whilst NIMs continue to be under pressure across the industry, DIB remains at healthy levels and at the higher end of the market, another remarkable feat and a testament to the bank’s ability to generate low cost funding whilst maintaining competitive

pricing on its financing book.

- The recent rights issuance has led to enhanced capitalization with overall CAR standing at 18%, and has created room for further advancement and penetration in existing clientele and industry sectors as we push forth our growth strategy for 2016.

- Given the solid performance so far and the robust balance sheet positioning, I believe that that we have the ingredients in place to navigate the economic challenges posed by the market and continue our performance leadership in line with the expectation

of all our stakeholders.

Financial Review

Income Statement highlights:

Total Income

Total income for the period ended June 30, 2016 increased to AED 4,236 million from AED 3,625 million for the same period in 2015, an increase of 17% driven primarily by growth in core businesses. Income from Islamic financing and investing transactions

increased by 20% to AED 3,126 million from AED 2,614 million for the same period in 2015. Fees and commissions have increased by 25% to AED 790 million compared to AED 630 million for the same period in 2015.

Net revenue

Net revenue for the period ended June 30, 2016 amounted to AED 3,356 million, an increase of 6% compared with AED 3,166 million in the same period of 2015. The increase is attributed to build up of core financing assets as well as growth in commissions

and fees.

Operating expenses

Operating expenses slightly increased by 7.0% to AED 1,152 million for the period ended June 30, 2016, from AED 1,080 million in the same period in 2015. The marginal increase is primarily due to growth in operational expenses in line with increased business

volume. Cost to income ratio remained stable at 34.3% compared to 34.1% for the same period in 2015, in line with guidance for the year.

Impairment losses

Impairment losses declined to AED 191 million compared with AED 276 million for the same period in 2015, an improvement of 31%, a clear sign of improving asset quality. With a 50 bps drop in NPL within the first half, the bank remains on target for the

guidance given for the ratio for 2016.

Profit for the period

Net profit for the period ended June 30, 2016, increased to AED 2,004 million from AED 1,801 million in the same period in 2015, an increase by 11%, stemming from higher revenues and declining impairment losses.

Statement of financial position highlights:

Financing portfolio

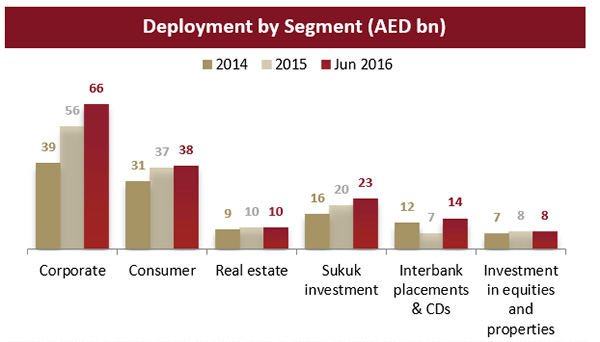

Net financing assets grew to AED 108.9 billion for the period ended June 30, 2016 from AED 97.2 billion as of end of 2015, an increase of 12%. This increase was supported by Corporate banking financing growth which rose to AED 76 bn (including commercial

real estate) and Consumer Banking which grew to AED 38 bn.

Asset Quality

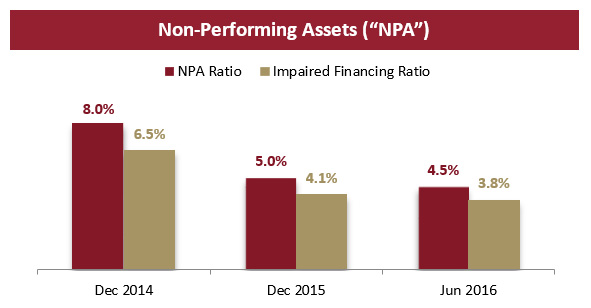

Non-performing assets have shown a consistent decline with NPL ratio improving to 4.5% for the period ended June 30, 2016, compared with 5.0% at the end of 2015. Impaired financing ratio also improved to 3.8% for the period ended June 30, 2016 from 4.1%

at the end of 2015. The improving NPLs and impaired ratio is primarily driven by recoveries in legacy portfolio as well as continuous growth in the quality asset book. With continued provisions, cash coverage improved to 100% compared with 95% at

end of 2015. Overall coverage ratio stood at 150% at the end of June 2016 compared to 148% at the end of December 2015.

Sukuk Investments

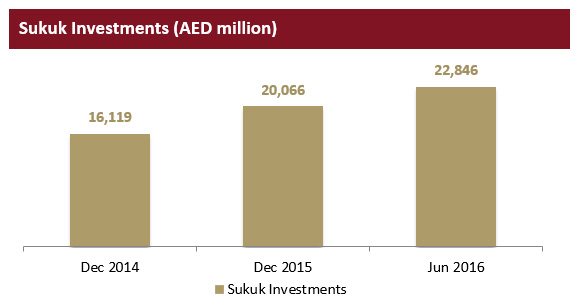

Sukuk investments increased by 14% for the period ended June 30, 2016 to AED 22.8 billion from AED 20.1 billion at end of 2015. The primarily dollar denominated portfolio consists of sovereigns and other top tier names many of which are rated, with average

yield across the portfolio of over 4%.

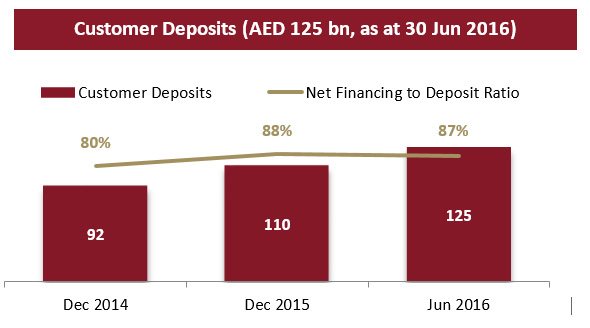

Customer Deposits

Customer deposits for the period ended June 30, 2016 increased by 13% to AED 125 billion from AED 110 billion as of end of 2015. CASA book increased by 15% to AED 51.3 billion compared with AED 44.5 billion in 2015. Investment deposits grew by 12% for

the period ended June 30, 2016 to AED 73.3 billion from AED 65.5 billion as at end 2015. Financing to deposit ratio of 87% as of June 2016 compared to 88% at the end of 2015, depicts continuing healthy liquidity.

Capital and capital adequacy

Capital adequacy ratio stands at 18.0% as of June 30, 2016, and T1 ratio at 17.8%, both ratios are well above regulatory requirement. The recent AED 3.2 bn rights issue gave a significant boost to T1 and overall CAR and was massively oversubscribed by

nearly 3 times indicating continuing investor interest and faith in the bank and its management.

* Regulatory Capital Requirements CAR at 12% and Tier 1 at 8%

Key business highlights for the 2nd quarter of 2016:

- Dubai Islamic Bank successfully raised additional capital through a rights issuance. The rights issue will increase the share capital of the bank to AED 4.9 billion from AED 3.9 billion and the transaction was nearly three times oversubscribed with

interest coming from both existing and new investors. The increased capital will allow the bank to implement its expansion and growth plans, strengthen its capital and improve DIBs liquidity position as it continues fortify its position in the

market.

- In June 2016, the Department of Economic Development (DED) in Dubai, and Dubai Islamic Bank (DIB), the largest Islamic bank in the UAE, announced the official launch of the first-ever ‘Consumer Card’ in the UAE, a co-branded credit card

dedicated to protect the rights of consumers and providing them with savings on their daily purchases. The card is an addition to the partnership initiatives being launched by DED along with the private sector and to the bank’s ongoing efforts

to enhance the shopping experience of consumers in Dubai, and across the UAE.

- Dubai Islamic Bank, the largest Islamic Bank in the UAE, reiterated its support for Emiratization through its participation at the 16th edition of “Careers UAE” held in May 2016, the leading national platform for both job seekers as well

as employers looking for skilled and promising Emirati talent. Emiratization remains a key component of the Bank’s philosophy to promote the economic and social development of the UAE.

- DIB outlined the group’s detailed growth strategy for its franchise in Pakistan, which is an integral part of the groups’ ever-expanding global operations. A new branding and identity was unveiled reinforcing the alignment of DIB Pakistan

with the group’s overall positioning.

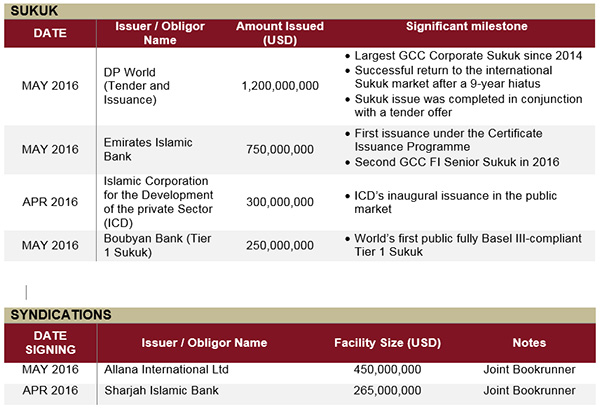

- Some key deals / transactions for the 2nd quarter:

1st half 2016 Awards: